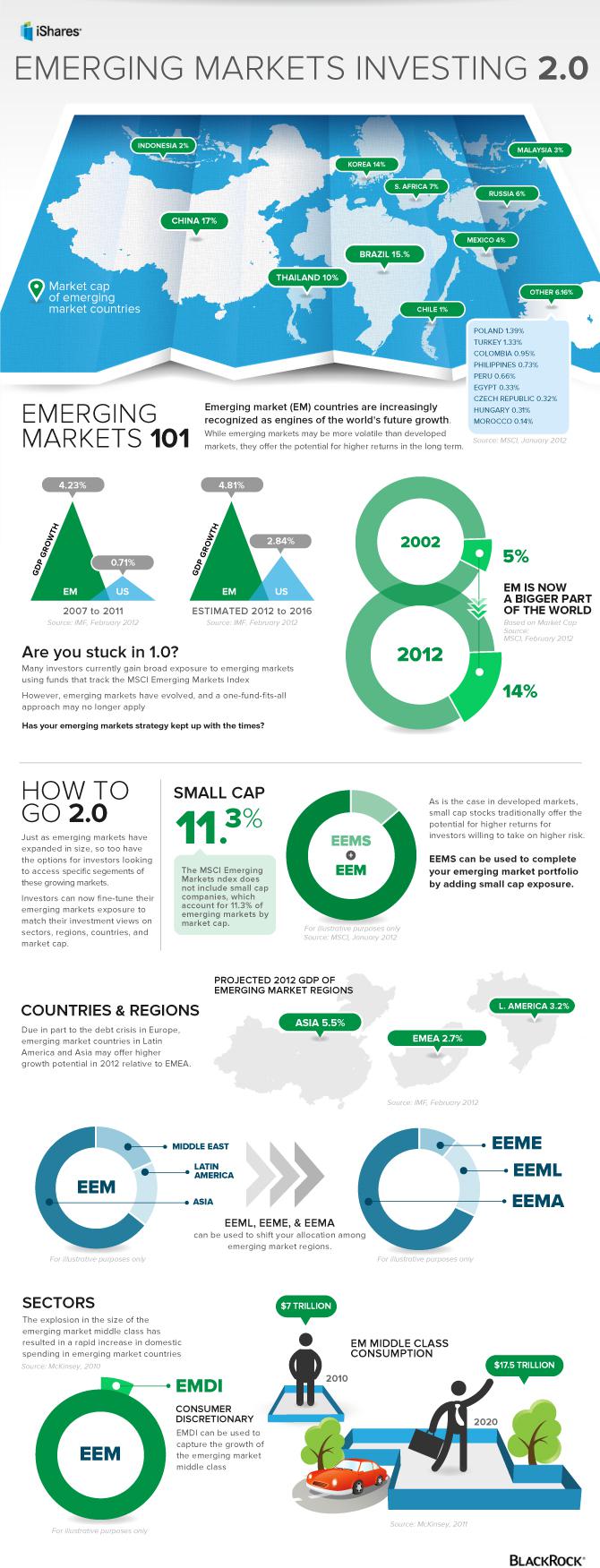

There’s been plenty of interest in the JP Morgan EM

Opportunities fund. Inevitably, it’s going to draw comparisons with the two bigger

GEM funds out there from First State and Aberdeen. So as an academic exercise,

I figured it’s worth comparing the performances of all three.

Richard Titherington, the face of JP Morgan EM Opps, is

listed as the manager since October 2009. So examining the time period of end-Sep

2009 to end-Feb 2013 gives about 3yrs of data to play with, with a rolling 12-month timeframe. to be fair,

|

| data: Lipper, in USD terms, dividends reinvested |

The two charts above say that the fund does well across the

ups and downs of the three years that Titherington has been managing the fund.

Most of the time, the performance beats the market, and when it does, it’s by a

bigger margin than when it doesn’t.

Performance alone says nothing about how he does it, neither does it say whether

he’ll repeat this in the future, which are arguably the two more interesting

questions. The next question then is how it compares against Aberdeen and First

State GEM funds.

|

| data: Lipper, in USD terms, dividends reinvested |

First State GEM leaders is a defensive machine, with a

larger margin of outperformance than JPMorgan EM Opps on the downside. It does

less well in stronger-than-average bull markets, compared with JPM EM Opps.

Still…a clean sheet in down markets is a tough act to follow, unless the fund

in question is one Aberdeen GEM fund.

Defensively, Aberdeen rivals First State GEM, with a clean

sheet in down markets. On the upside, Aberdeen GEM in the past three years

tends to beat the market, but relative to the other two funds, by a smaller

margin. Again, clean sheet = tough act.

So from an investor’s point of view, the question of which

fund to choose boils down to whether one is looking for a fund that performs

well in up markets and down markets, or one that performs well in up markets,

but better in down markets. All three are solid performers, with Aberdeen and

First State holding

an edge when markets

head south.

Clearly, there’s a lot of interest in the

EM story, and a lot of people

are filling up the space, which is great for choice. But I reckon there

will be more thematic funds coming up. We already have a few

EM

small

cap

funds in the space, infrastructure spending is big in India, and China’s

consumption story has already inspired a consumption-themed fund or two.

Of course, so much interest in a relatively immature market

does raise caution in several better known bears. Andy Xie for instance, has started

writing about a BRIC bubble:

‘Whenever there is a hot concept like BRIC, there is a bubble. There has never been an exception.’

{kind=link}